The May ISM manufacturing index came in at 49, below expectations of 51. Although this signals that slightly more firms reported that conditions had weakened from the prior month, this does not suggest that overall economic activity declined. As the chart above suggests, a reading of 49 is consistent with economic growth of 1.5 - 2%.

The prices paid component was neutral, suggesting that firms are not experiencing significant inflation or deflation pressures.

The employment component was also neutral, suggesting no future pickup or deterioration in manufacturing activity. For the most part, firms are not expecting any meaningful change in the environment.

The softening of activity in the U.S. manufacturing sector is offset to a degree by some marginal improvement in manufacturing activity in the Eurozone.

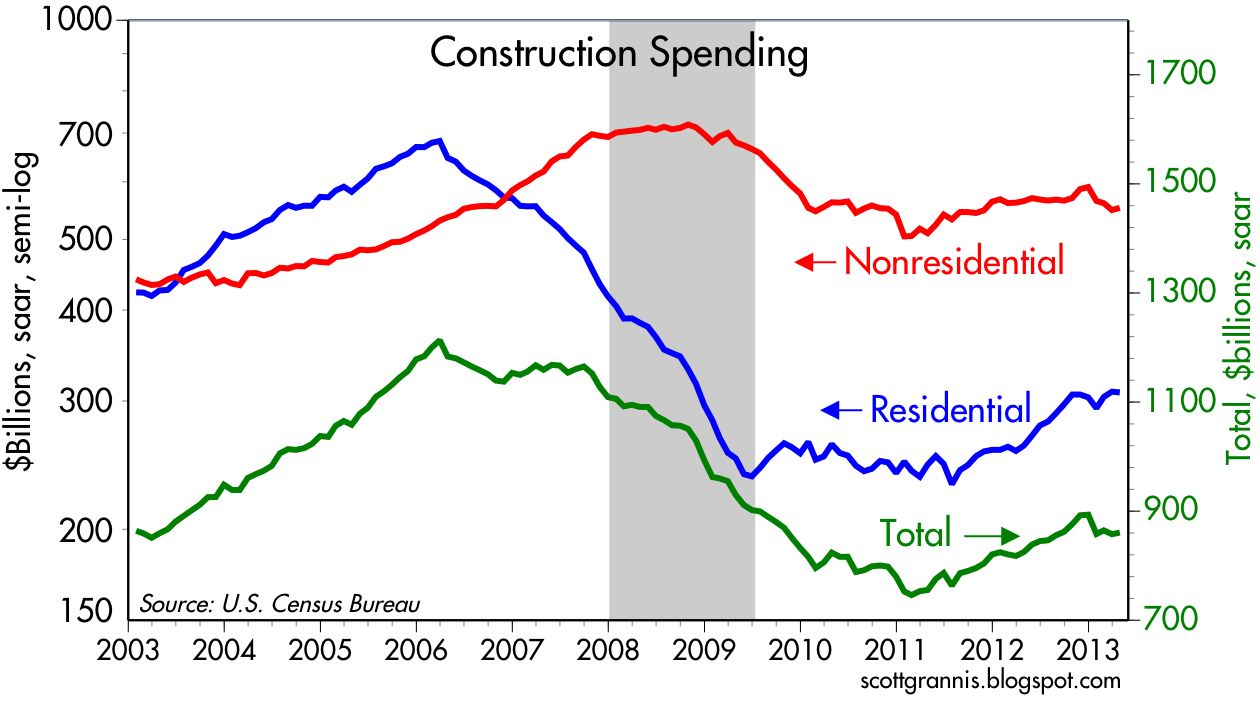

Construction spending in April rose a modest 0.4%, on top of modest upward revisions to the past few months' data, leaving total spending 4.3% higher over the past year. Nothing to get excited about here.

Construction spending represents about 40% of the broader "domestic private fixed investment" category, which includes equipment and software. Fixed investment has rebounded in the past three years from extraordinarily depressed levels, and this tracks well with the decline in the unemployment rate.

It's steady and (disappointingly) slow as she goes. Business confidence and willingness to invest needs to improve a lot more if we are to see any meaningful improvement in the economic outlook. So far there is no sign of that.

Tidak ada komentar:

Posting Komentar