Recent economic data continue to show no sign of any emerging weakness or unusual strength in the U.S. economy. The economy is likely continuing to grow at about a 2% pace, which is the average pace of the current business cycle expansion. Despite any notable changes in the health of the economy, the market has rather suddenly been gripped by fear that a tapering of the Fed's Quantitative Easing program—not a reversal, just a slower pace of asset purchases—puts the economy at risk. This fear is based on the assumption that the recovery has been primarily driven by QE, an assumption I think is unfounded. I see no logical connection between the Fed's purchases—which amount to swapping T-bill substitutes for notes and bonds—and the creation of new jobs. As I argued months ago, the Fed is not "printing money."

If there is any connection between QE and economic growth, it is that both are unprecedented: we've never seen the Fed purchase assets of such magnitude, and we've never seen such a slow-growing economy after such a deep recession. Indeed, it might make more sense to believe that QE has actually retarded the economy's growth—and that therefore a tapering of QE might actually boost growth—rather than to worry that a slow-growing economy might get even slower if the Fed begins to taper its purchases of notes and bonds.

Some brief notes on today's data releases:

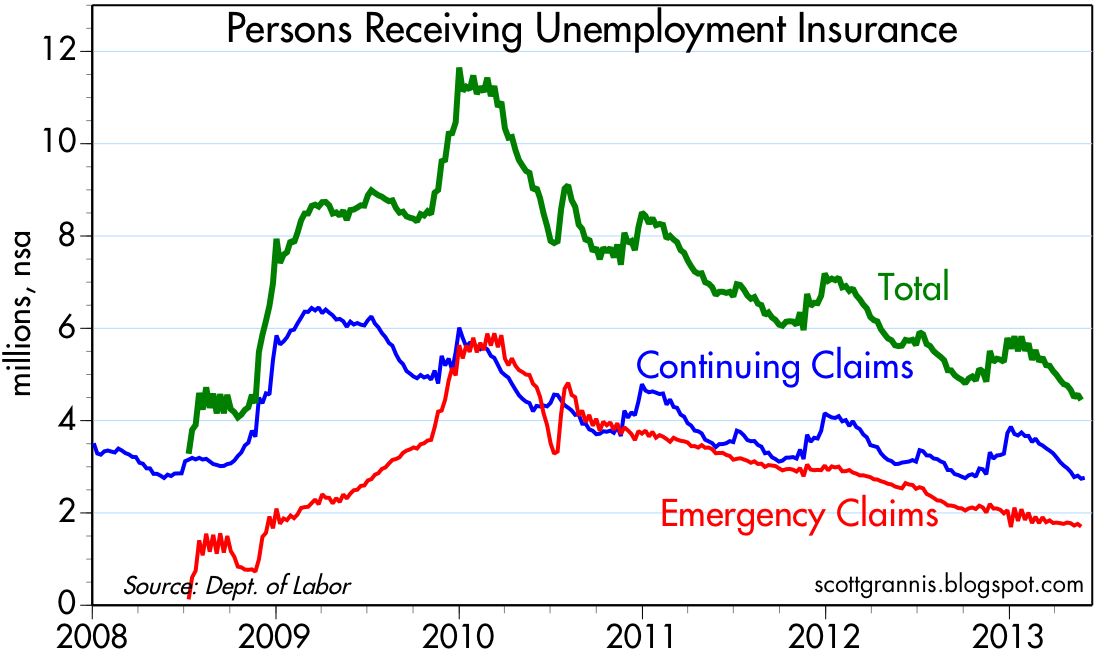

Weekly claims for unemployment continue their downtrend. This suggests the labor market is getting more resilient by the day, as employers have done just about all the cost-cutting they need to.

Relative to the size of the workforce, layoffs have rarely been lower than they are today.

The number of people receiving unemployment insurance is down almost 21% in the past year. This continues to be one of the biggest changes on the margin in the U.S. economy, and it is a positive, since it increases the incentives for people to find and accept employment.

May retail sales were stronger than expected (+0.6% vs. +0.4%). To date there is no sign that the expiration of the payroll tax holiday (which caused withholding taxes to increase beginning in January) has had any significant impact on consumer spending. Real retail sales are up about 3.3% in the past year, and in the past six months they are up at 2.7% annualized pace.

The main problem with the economy has been a failure to thrive. Unemployment remains quite high, and the economy is operating at much less than its capacity. As the chart above suggests, retail sales are a little more than 10% below where they otherwise could have been if this had been a normal recovery. This, combined with the fact that inflation remains relatively low, is hardly evidence that the Fed has artificially pumped up the economy with QE.

Tidak ada komentar:

Posting Komentar