The May employment report shed no new light on the state of the labor market. For the past two years, and for the past six months, the private sector has been adding jobs at about a 2% annual pace. Consideriing the huge job losses that came with the Great Recession, that adds up to the slowest recovery in the jobs market in modern times, and it's the source of lots of angst and hand-wringing. Things could be a lot better, but at least jobs are growing. There is no boom or double-dip recession out there, and neither appear likely for the foreseeable future. It's simply modest-to-moderate growth.

But as I've been asserting for a long time,

avoiding recession is all that matters when the yield on cash is zero. If the labor market continues to grow at the pace of the past two years, investors who avoid cash are likely to do better than those who hold cash, because the yield on non-cash assets is much higher. Zero-interest cash only pays off if the economy suffers a disruption that reduces cash flow, increases default risk, and/or impairs profits (since any of those is likely to depress the prices of risk assets). As time passes and the economy continues to grow, the cumulative outperformance of non-cash assets will increase the world's temptation to reduce cash holdings, and that will eventually show up as higher prices for risk assets.

The Fed will eventually succeed in reflating the economy, but not by "printing money." Reflation requires convincing the world that holding lots of cash (and relatively safe assets like short-term Treasuries) doesn't make sense. To date, the Fed has been working hard to supply bank reserves to the world in order to satisfy what has proved to be an extraordinary demand for cash and cash equivalents. As the demand for cash declines, the Fed should be able to reverse its Quantitative Easing with no adverse consequences, because it will be trading higher-yielding assets (e.g., notes and bonds) for the cash the public has tired of holding. The key to reversing QE is thus a declining demand for money, and we are seeing the early signs of that in the recent rise in real yields on TIPS and nominal yields on Treasuries (see chart above). Rising yields on relatively safe assets such as 5-yr T-notes and 5-yr TIPS are the flip side of falling prices (i.e., falling demand). Put another way,

rising real yields on TIPS are a sign of increased confidence in future economic growth (or decreased pessimism). Increased confidence in the future comes hand in hand with reduced demand for cash and cash equivalents.

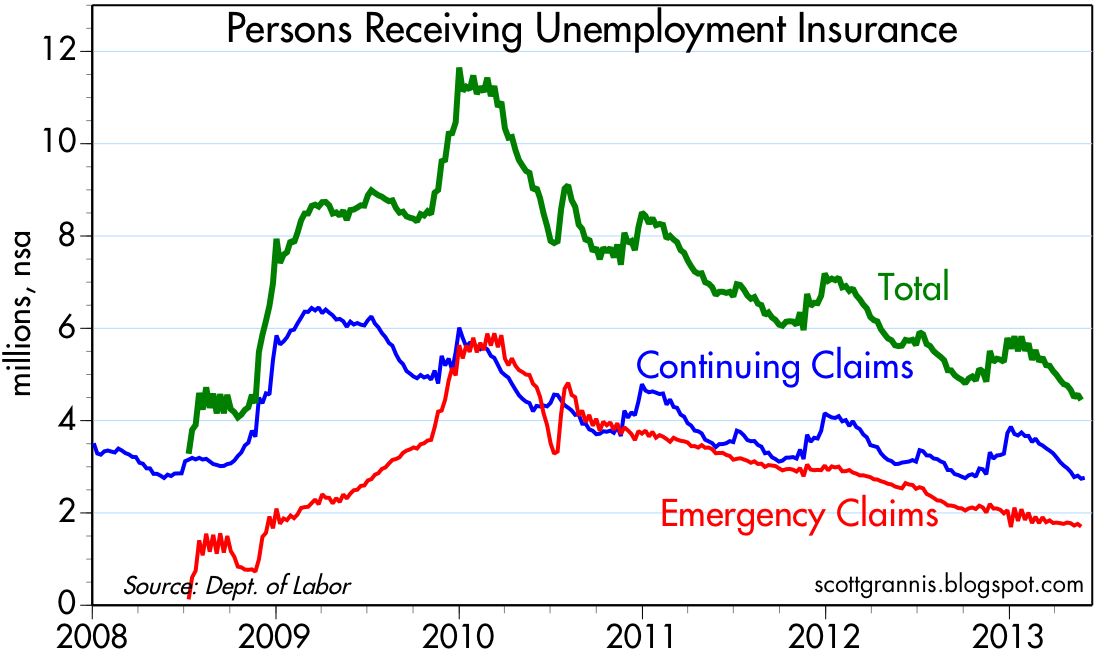

But back to the labor market. As the chart above shows, the economy continues to add jobs. Since the low in early 2010, the private sector has created between 6.7 and 6.9 million new jobs, according to the government's two employment surveys. There is no sign that this growth is ebbing or accelerating.

Overall jobs growth has been a bit slower than the growth of private sector jobs, because the public sector has been shedding jobs for the past four years. This is actually a healthy development, since the private sector is generally more efficient than the public sector, and since the public sector had grown like topsy over the past decade or so. A shrinking public sector frees up resources for the more productive private sector, so over time that should boost growth somewhat. We probably haven't seen the end of this shrinkage either.

Private sector jobs growth has been averaging just over 2% a year for more the past two years. This is almost exactly the same pace as jobs growth in the mid-2000s. In a sense, it's business as usual.

The most unusual thing about this recovery is the very slow growth of the labor force over the past four years. Instead of growing about 1% per year (in line with growth in the population), labor force growth has been extremely weak, and has posted only 0.4% growth in the past year. Demographics (e.g., the aging and retirement of baby boomers) can explain some of this slowdown, but it's likely that the large increase in transfer payments since 2008 (e.g., food stamps, social security disability, emergency unemployment benefits) has played a role as well. When compassionate government doles out money to assuage the victims of a recession, it inadvertently acts to retard the recovery because it reduces the incentives to get back to work. It's also likely that the big increase in regulatory burdens in recent years (e.g., Dodd-Frank, Obamacare, EPA rules) has created disincentives for businesses to expand, thus limiting job opportunities and leaving many would-be workers discouraged. Higher marginal tax rates haven't helped either, since they are a disincentive to work and invest. The economy is growing at 2%

despite all these headwinds.

Does the Fed really think that buying $85 billion worth or Treasuries and MBS each month and paying for them with bank reserves will change this relatively slow-growth picture? How exactly will more bank reserves lead to more job creation? It's not obvious to me.

As the chart above shows, there is no evidence that the Fed's Quantitative Easing efforts have resulted in any unusual amount of money growth. The M2 measure of the money supply, arguably the best, has grown only slightly faster than 6% per year since the Great Recession. That growth is easily explained by strong money demand: the vast majority of the growth in M2 in the past 4-5 years has come from an increase in bank savings deposits. At the same time, virtually all of the Fed's $2.3 trillion worth of purchases of Treasuries and MBS have gone to support increased currency in circulation and excess reserves. Banks now hold $1.9 trillion of excess reserves at the Fed; they are presumably happy to do so because reserves pay interest and are thus effectively a substitute for T-bills. Banks are still quite risk averse as is the public, since households continue to

deleverage. Hardly any of the flood of new bank reserves has been used by banks to increase lending and expand the money supply. Currency in circulation is up more than $0.34 trillion since Q3/08, largely because people all over the world want to hold more dollars under the mattress, so to speak.

This can't go on indefinitely. At some point attitudes toward risk will change, and the demand for safe assets and cash will decline. Bank lending will increase. Money supply growth will increase. Nominal GDP growth will increase. The prices of risk assets will rise further. All of these will be signs that the Fed should begin to reverse QE. As mentioned above, there are already tentative signs of this, and

one more non-recessionary jobs report such as today's only makes it more likely that this process is getting underway. I'm reminded of my

post last March:

... the biggest risk we all face as a result of the Fed's unprecedented experiment in quantitative easing is the return of confidence and the decline of risk aversion. If there comes a time when banks no longer want to hold trillions of dollars worth of excess bank reserves for whatever reason (e.g., the interest rate the Fed is paying is no longer attractive, or the banks feel comfortable using their reserves to ramp up lending, or the public no longer wants to keep many of trillions of dollars in bank savings deposits), that is when things will get "interesting."

I suspect that the Fed has been engaged in a bit of false advertising, claiming that it is buying billions of Treasuries and MBS in order to lower interest rates and thereby goose the economy. The dirty secret is that monetary policy can't create or stimulate growth, it can only facilitate growth. As I

discussed the other day, interest rates are now higher than they were when QE3 started late last year. Paradoxically, rising interest rates are the clearest sign that QE has achieved its real purpose. In reality, all the Fed is doing is satisfying the world's demand for safe assets: exchanging bank reserves for notes and bonds. There's nothing wrong with that, and if they hadn't done this we'd be in a world of hurt—there would have been a shortage of safe money and that could have led to deflation and worse. The Fed has satisfied the world's demand for safe assets, but there is no evidence at all that the Fed's actions have translated into more jobs or faster growth. The economy has been growing all along the old-fashioned way: by adjusting to new realities, by working harder and more efficiently, and by investing more, in spite of all the obstacles. Economic growth and new jobs are not created by adding bank reserves to bank balance sheets.

The issue right now is when the Fed will begin to "taper" its QE program, and whether this will hurt the economy or not. The Fed has suggested that the unemployment rate needs to fall much further before they start to unwind QE, but we're not likely to see a 6.5% unemployment rate anytime soon if current trends continue—it could take another year.

Meanwhile, there seems to be growing unease among FOMC members with the obvious progress the economy is making. It's risky to keep the monetary pedal to the metal year after year when the economy has already demonstrated the ability to create jobs at the same pace as it did in the mid-2000s.

I think this explains why the Fed is trying now to accelerate its transition to an unwinding of QE, well in advance of the economy hitting the targets the Fed had previously proposed. It's a tacit admission that the purpose of QE wasn't really to create more jobs, it was to satisfy the world's demand for safety in uncertain times. Now that the economy has demonstrated the ability to grow for the past four years, and now that the public's demand for safe assets is beginning to decline (witness also the big drop in gold prices in recent months), QE is no longer necessary. Godspeed. It will not be missed. Higher interest rates do not necessarily pose a threat to growth, they are a natural result of growth.