It's also very important to note the message of TIPS. Real yields on TIPS have risen a bit more than nominal yields on Treasuries, which means that the market's inflation expectations have declined a bit. That's another way of saying that the rise in Treasury yields has been dominated by a rise in real yields, not by a rise in inflation or inflation expectations. Higher real yields confirm the message of stocks: what has been happening over the past year is an improvement in the economic fundamentals. Even though (I repeat) this remains the most miserable and weakest recovery in history.

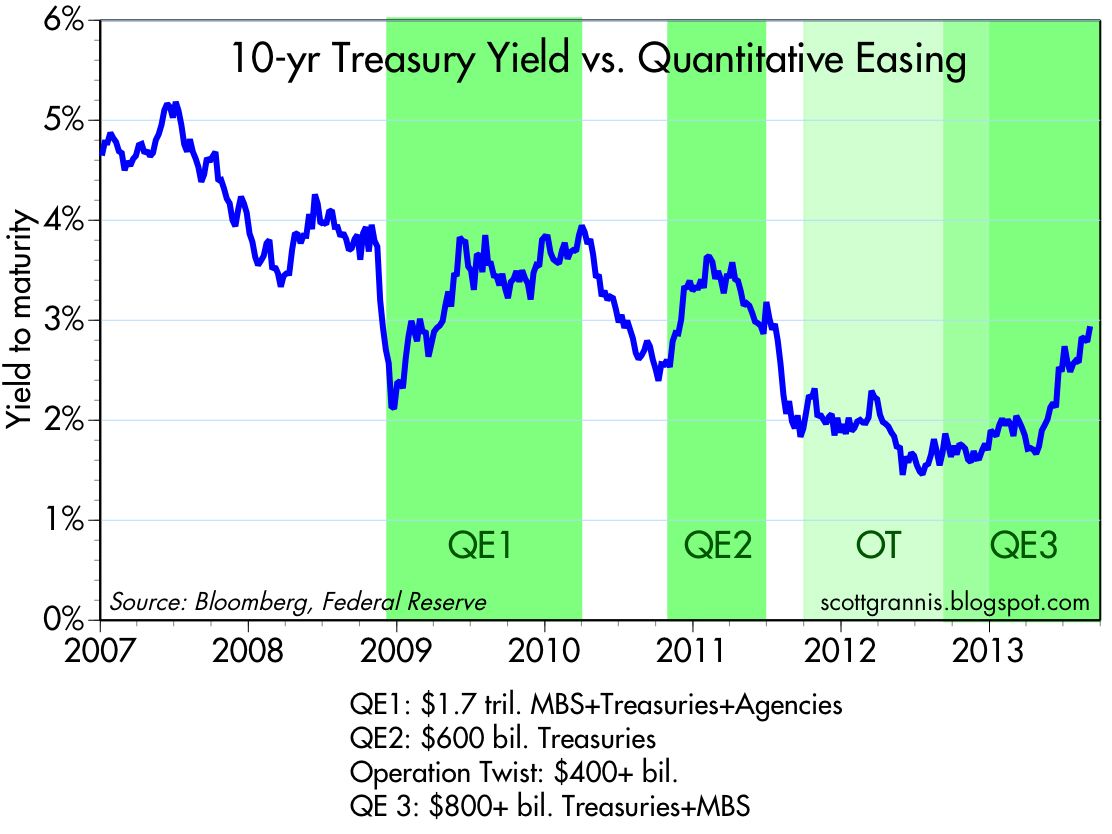

UPDATE: Reader "Sil Sanders" notes that it's not obvious from my charts and my explanation (admittedly brief) above that QE has failed to keep rates low. For a more complete explanation, see my post from last month, "Why QE was a successful failure." The chart below is an updated version of one of the charts from that post:

As I said back then, 10-yr yields ended up higher at the end of each QE program, and were unchanged at the end of Operation Twist. Yields only fell during periods when the Fed was not engaged in buying bonds—surely a counterintuitive result.

As I argued in the post linked above, and on many other occasions (here, here, here, and here), the only result the Fed could hope to achieve with QE was to raise, not lower rates, by responding to the world's demand for safe assets and thus alleviating a potential liquidity shortage which likely would have led to a weaker economy. As I've argued many times in the past, interest rates are fundamentally determined by the market's perception of economic growth and inflation. The chart above shows how real yields on TIPS tend to track the economy's growth rate, and the chart below shows how nominal yields track inflation.

I would argue that it makes much more sense to view the decline in yields over the past 5-6 years as a response to the market's expectation that economic growth would be very weak and inflation very low, rather than as the result of the Fed's bond purchases, which after all only represented a small fraction of the outstanding amount of bonds and MBS. That same logic, combined with a modest decline in inflation expectations in recent months, argues that the recent rise in yield is therefore the result of the market's improving expectations for economic growth in the years to come. As the second chart above shows, however, current 10-yr yields suggest the market now feels comfortable with economic growth of about 1% per year. Not too long ago, 10-yr yields were consistent with growth expectations of zero or even a modest recession. Even with the recent and rather impressive rise in 10-yr yields, the market's outlook for future economic growth is still quite modest.

One final point: if I'm right, and QE never artificially lowered rates nor directly stimulated the economy, then the "tapering" and eventual reversal of QE should not pose any threat to the economy as so many seem to fear, so long as the Fed's efforts have satisfied the world's demand for "safe assets."

Tidak ada komentar:

Posting Komentar